For many of us, hitting the big 50 is when our financial landscape starts to change dramatically. As we start looking towards retirement, our attitude to risk changes, our financial liabilities and responsibilities change, and we may even consider downsizing. Let's explore five ways your finances may change when you hit 50.

1. Traditional mortgages can be out of reach

As you get older, you may find it harder to find a good mortgage deal. Your financial situation can change, as your income could drop as you approach retirement. Typically, the lending criteria are stricter for older borrowers. You're likely to only find mortgages with shorter repayment periods and might find lenders offering fewer deals. Despite these difficulties, the UK mortgage market has options for over 50s.

Downsizing

Many of us approaching retirement have lived through and benefitted from a UK housing boom which began in the 1980s. As children fly the nest to start their own families, new careers and new challenges, many parents are left with large multi-bedroom properties. Consequently, downsizing is a serious consideration, often allowing homeowners to acquire a new property mortgage-free. However, there are other options for those looking to extract equity from their property.

Lifetime mortgages and home reversion schemes

There has been a significant increase in the availability of lifetime mortgages and home reversion schemes targeted at those approaching retirement. The lifetime mortgage option allows you to release equity without any monthly payments. Instead, interest is rolled up and repaid with mortgage capital upon the sale of your property, which happens on your death or move into full-time care.

Home reversion schemes allow you to sell a percentage of your property to a third-party investor. While often at a significant discount to the market value, this offers another way to release equity from your home. Before you die or move into full-time care, you will live rent-free in the property, with the investor receiving their share of eventual sale proceeds.

2. Life insurance for over 50s

Whether looking to cover outstanding debts or leave your partner & family financially secure upon your death, life insurance for over 50s is a serious consideration for many. You will notice many insurance companies offer over 50s life insurance with no medical. This can be especially attractive for those with underlying medical issues. However, it is essential to compare these premiums with other insurance options.

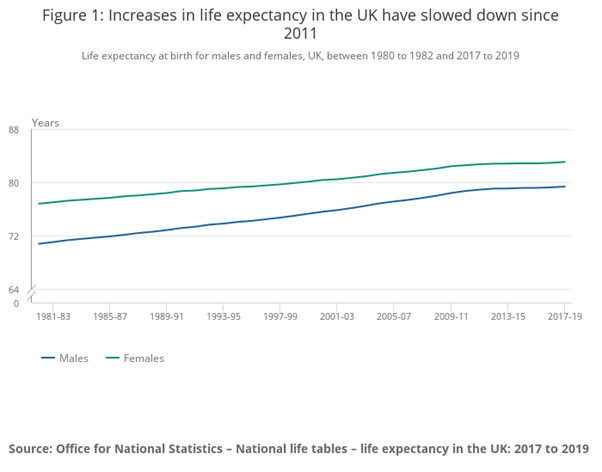

The life expectancy curve for the UK population has flattened out in recent years. It currently stands at 83.1 years for women and 79.4 years for men.

Consequently, insurance companies can now offer desirable terms to over 50s, knowing average life expectancy is not expected to increase materially in the short term. This has become an incredibly competitive area of the insurance market, and it is more critical than ever to take professional financial advice. Make sure your life insurance terms and conditions dovetail as neatly as possible with your life circumstances.

3. Inheritance tax planning is essential

While not necessarily the most comfortable subject to discuss as you approach the “best years of your life”, inheritance tax planning is vital. Currently, the inheritance tax threshold is £325,000 (£650,000 for a couple). One of the simplest means of retaining control over your assets is to consider gifting in life.

Gifting assets in life

There are various exempt gifts such as wedding/civil ceremony gifts, Christmas and birthdays, charitable contributions and assistance with third-party living costs. You can also give away £3,000 worth of gifts per annum without leaving any inheritance tax liabilities for beneficiaries of your estate. However, if you're looking to gift assets above this level before your death, you may create a future liability on your estate. The following table details inheritance tax taper relief, which allows the government to draw recent gifts back into your estate:

| Duration between gift and death | Inheritance tax liability |

Less than three years | 40% |

3 to 4 years | 32% |

4 to 5 years | 24% |

5 to 6 years | 16% |

6 to 7 years | 8% |

7 or more years | 0% |

If you die within seven years of gifting assets to third parties, and your estate is liable to inheritance tax, HMRC will charge tax at the above tapered rates on each gift. It is, therefore, essential to seek professional financial guidance to mitigate any future potential tax liability. In many cases, the cost of this advice will pay for itself!

4. Maximise your pension assets for the future

It makes sense to prepare for retirement, with many of us beginning to focus on this as we approach 50. You may have defined benefits and contributions pension pots and the state pension to fund your retirement lifestyle. As you approach 50, it is essential to:

- Make full use of your pension contribution allowance

- Consider other tax-efficient vehicles such as ISAs

- Review your risk/reward investment profile

The UK government introduced a range of pension reforms back in 2015. These reforms give individuals more flexibility around pension drawdown and investments. However, many people still follow the traditional pension investment path. This involves switching from volatile and medium-high risk investments to more sedate secure investments such as bonds and quasi-cash asset classes.

In some circumstances, you may be able to claw back unused pension contribution allowances from previous years. However, this subject is not straightforward, and it is sensible to take professional financial advice.

If you are unsure about your future state pension entitlement, you can check this on the UK government website.

5. Are you claiming your benefit entitlements?

According to Age UK, a staggering £3.5 billion in pension credit and housing benefit remains unclaimed by older people each year. It would appear that a mixture of pride and a lack of awareness has brought us to this scenario. As you approach retirement, you must be aware of your benefit entitlements and ensure you claim them. While some payments may be means-tested, you could be entitled to one or more of the following benefits:

- Winter Fuel Payment

- Public transport

- Housing

- TV licence

- Council tax

- Employment/support allowance

- Pension credit

- Income support

- Universal Credit

These are just some government benefit payments you may be entitled to, now and in later life. While there have been significant improvements in the number of pensioners living in poverty over the last 20 years, there are still 1.9 million pensioners struggling to make ends meet. While many may struggle in silence, billions upon billions of pounds of benefits go unclaimed each year.

Planning for retirement

It is never too soon to plan for your retirement. That said, once you hit 50, you may see a significant change in your financial landscape, assets, liabilities and family life. Therefore, it is essential to look to the future, mitigate potential tax obligations, maximise your income, and ensure that you claim all you are entitled to. Over the last 20 years, we have seen a significant reduction in impoverished pensioners. However, pressure on incomes and the ever-rising cost of living will certainly push more pensioners into poverty in the short term.

There has never been a greater need for financial planning as you approach 50 and start to look forward to your retirement.

Stuart Carswell, Director at Pareto Financial Planning, agreed with these sentiments. He told Pension Times: “The earlier you start planning for your retirement the better. You increase your chances of achieving your desired lifestyle in retirement and will have a better idea of at what age you can stop working. In the current financial climate planning ahead has never been so important. Reviewing plans and adjusting to economic changes is just as important as creating a plan in the first place.”